BOP Cost Calculator

Your Business Details

Your Results

Your Coverage Options

Based on article data: BOPs save 20-30% on average compared to separate policies.

Starting a small business is hard enough without worrying about whether you’re covered if something goes wrong. That’s where a Business Owner’s Policy (BOP) comes in. It’s not magic, but it’s close-combining the most important types of insurance into one simple, affordable package. For startups with a physical location, inventory, or customers walking through the door, a BOP isn’t just smart. It’s often the only insurance you need to start off right.

What Exactly Is a Business Owner’s Policy?

A BOP isn’t a new kind of insurance. It’s a bundle. Think of it like buying a meal deal instead of ordering each item separately. You get three core protections in one policy:

- Commercial property insurance-covers your building, furniture, computers, inventory, and equipment if they’re damaged by fire, theft, storms, or other covered events.

- General liability insurance-protects you if a customer slips on your floor, gets hurt by your product, or sues you for something like copyright infringement in your ads.

- Business interruption coverage-pays for lost income and ongoing expenses if you have to close temporarily because of a covered disaster.

It’s designed for small businesses with low to moderate risk. That means if you run a bakery, a boutique, a local repair shop, or even a home-based consulting business with a dedicated office space, a BOP likely fits you. According to the Insurance Information Institute, over 80% of small businesses that qualify for a BOP choose it because it’s simpler and cheaper than buying each policy alone.

Why Startups Love BOPs

Startups are tight on cash and time. Managing five different insurance policies? Not ideal. A BOP cuts the paperwork, the billing, and the confusion. One payment. One renewal date. One point of contact when you need help.

Here’s what real startup founders say:

- “We opened our coffee shop last year. The landlord asked for proof of insurance. We got a BOP in 20 minutes online. Showed them the certificate. Done.”

- “I was paying $1,200 a year for separate property and liability policies. Switched to a BOP-now I pay $780. Same coverage, less hassle.”

- “We got hit by a storm. The roof leaked. Our BOP paid for the repairs and covered lost sales while we cleaned up. No fight with the insurer. Just got paid.”

That’s the real value. It’s not about having the most coverage. It’s about having the right coverage-without overpaying or missing critical pieces.

What a BOP Doesn’t Cover (And Why It Matters)

Here’s where people get burned. A BOP is great-but it’s not everything. If you assume it covers all risks, you’re setting yourself up for a nasty surprise.

These are always excluded from standard BOPs:

- Workers’ compensation-if you have employees, you need this separately. It’s required by law in almost every state.

- Professional liability (errors & omissions)-if you give advice, design websites, consult, or provide services, this covers you if a client sues you for a mistake. A BOP won’t touch this.

- Commercial auto insurance-any vehicle used for business needs its own policy.

- Cyber liability-if you store customer data, use online payments, or rely on cloud software, you’re at risk. Most BOPs don’t cover data breaches or ransomware attacks.

- Health or disability insurance-these are personal protections, not business ones.

For example, a startup that builds mobile apps might think a BOP covers them. But if a client claims their app crashed and lost their data, that’s a professional liability claim. No BOP will help. You need E&O insurance.

Same with a food delivery service. If you use your own car to deliver, a BOP won’t cover an accident. You need commercial auto.

Who Should Skip a BOP?

Not every startup needs a BOP. If your business looks like this, you might be better off with targeted policies:

- You work entirely remotely-no office, no inventory, no customers coming to you.

- You’re a freelancer or solopreneur offering services like graphic design, coaching, or writing.

- Your biggest risk is a client suing you for bad advice, not a broken window.

- You use vehicles regularly for business.

In these cases, you might only need general liability and professional liability. Buying a BOP means paying for property coverage you don’t need. That’s wasted money.

One founder in Asheville ran a digital marketing agency from her apartment. She bought a BOP because her friend said it was “the standard.” She paid $900 a year. When she got sued for a failed campaign, her claim was denied. She ended up paying $3,500 out of pocket for legal fees. She switched to standalone liability and E&O coverage-now she pays $550 a year and is fully protected.

How to Get the Right BOP for Your Startup

Getting a BOP is easy. Getting the right one takes a few smart steps.

- Know your risks. What could go wrong? Fire? Theft? A customer slipping? A lawsuit over your website copy? List them.

- Know your assets. What’s in your space? Computers, furniture, tools, inventory? Estimate their replacement value. Don’t guess-take a photo inventory.

- Check your lease or contracts. Landlords and clients often require minimum coverage amounts. Make sure your BOP meets those.

- Ask about endorsements. Most insurers let you add coverage for a small extra cost. Common ones for startups: cyber liability, data breach, equipment breakdown, and flood insurance (if you’re in a flood zone).

- Compare quotes. Don’t just go with the first offer. Use online platforms like Insureon or Coterie to compare A-rated carriers. You can get quotes in under 15 minutes.

Pro tip: If you’re working from home, make sure your policy covers home-based business use. Some policies exclude it unless you specifically ask.

Costs and Savings

How much does a BOP cost? It varies, but here’s what most startups pay in 2025:

- Low-risk businesses (consultants, small retail): $500-$800/year

- Medium-risk (restaurants, repair shops, salons): $1,200-$2,500/year

- High-risk or larger spaces (manufacturing, warehouses): $3,000+

Compare that to buying property and liability separately: you could pay $1,000-$1,500 just for liability, and another $800-$1,200 for property. Bundled? You save 20-30% on average.

And remember-most policies include business interruption coverage at no extra cost. That alone can save you thousands if you’re forced to close for a week.

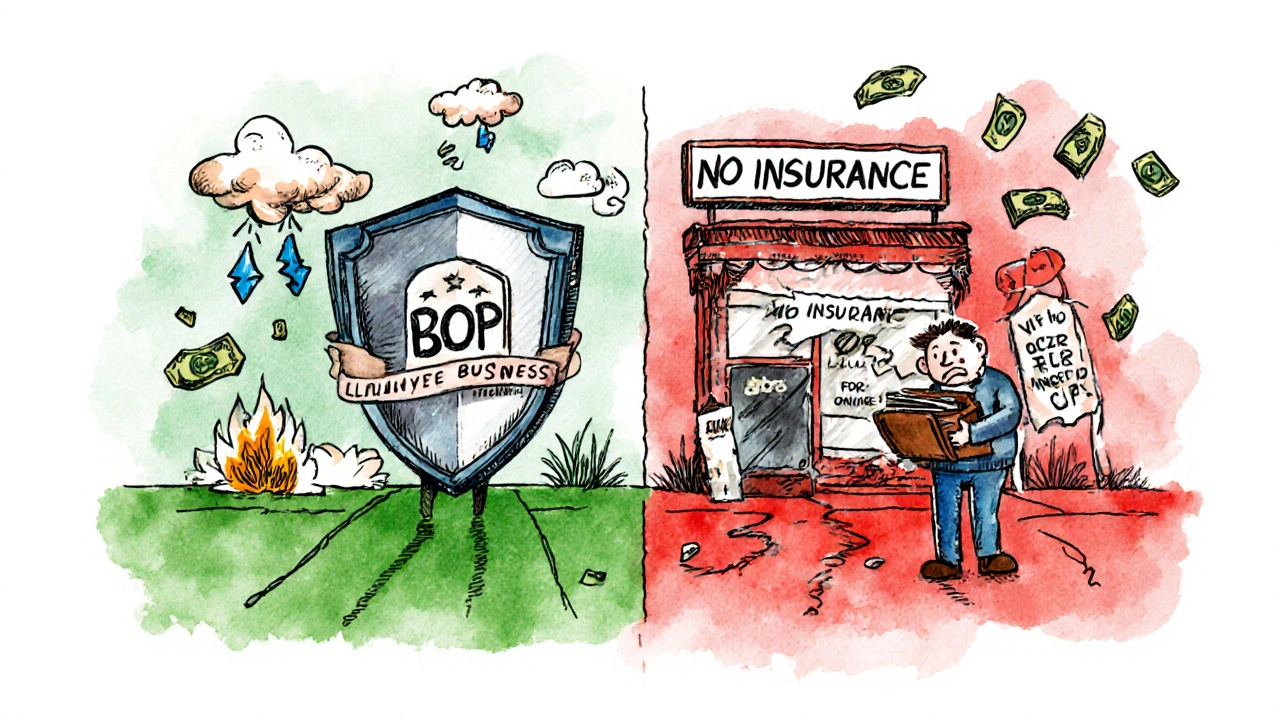

What Happens If You Don’t Get Covered?

One bad accident or lawsuit can wipe out a startup. In 2024, the average liability claim for a small business was $12,500. Property damage claims averaged $18,000. Without insurance, you’re paying out of pocket.

And it’s not just money. If you don’t have proof of insurance, you can’t sign leases, work with big clients, or even get approved for business loans. Banks and landlords check. They won’t take a chance on you without it.

One startup in North Carolina lost their entire inventory in a warehouse fire. They didn’t have insurance. They closed within three months. Their competitor, who had a BOP, got paid for the loss, rebuilt, and doubled their sales the next year.

Final Thoughts

A BOP isn’t a luxury. For most startups with a physical presence, it’s a baseline requirement. It’s not the only insurance you’ll ever need-but it’s the one you need first. Get it right, and you protect your business, your savings, and your peace of mind.

Don’t wait for a disaster to realize you’re exposed. Talk to a provider. Get a quote. Compare your options. Then make a decision. It takes less time than your morning coffee.

Is a BOP enough for a startup with employees?

No. A BOP doesn’t cover workers’ compensation, which is legally required if you have employees. You’ll need to add a separate workers’ comp policy. Some insurers let you bundle it with your BOP, but it’s not included by default.

Can I get a BOP if I work from home?

Yes. Many BOPs cover home-based businesses, but you must disclose that you’re operating from home. Some policies exclude home-based use unless you specifically request it. Make sure your policy includes coverage for business equipment stored at home and liability for clients visiting your residence.

Do I need cyber liability if I have a BOP?

Almost certainly. Standard BOPs don’t cover data breaches, ransomware, or phishing attacks. If you store customer information, accept online payments, or use cloud software, you’re at risk. Adding cyber liability as an endorsement costs $200-$600 extra per year and can save your business from a catastrophic loss.

How do I know if my business qualifies for a BOP?

Most insurers require your business to have fewer than 100 employees, less than $3 million in annual revenue, and a physical location (even if it’s home-based). If you’re a service-based business with no inventory or storefront, you may still qualify-but you’ll want to confirm with your provider that your risks align with standard BOP coverage.

Can I customize my BOP after buying it?

Yes. Most BOPs are flexible. You can add endorsements like cyber liability, equipment breakdown, or business auto coverage later. Just contact your insurer. You don’t have to wait for renewal. Many providers offer online updates, and changes often take effect within 24 hours.

Comments (3)

Laura W

OMG YES. I got my BOP last year for my tiny Etsy studio and it was a GAME CHANGER. Landlord asked for proof? Sent the PDF. Got hit by a freak hailstorm that shattered my window and ruined half my inventory? Insurer paid out in 72 hours. No drama. No ‘we’ll get back to you.’ Just cash. And the best part? I saved 30% vs buying property + liability separately. If you’ve got a physical space-even a corner of your apartment-get this. Stop overthinking it. You’re not ‘too small’ to need it-you’re too small to afford NOT having it.

Graeme C

Let me be brutally clear: anyone who thinks a BOP is ‘enough’ is walking into a minefield with blindfolds on. I’ve seen three startups implode because they assumed ‘bundle = complete.’ Cyber liability? Excluded. Professional liability? Excluded. Workers’ comp? Excluded. If you’re a service-based founder-graphic designer, consultant, coder-you’re paying for property coverage you don’t need while leaving yourself exposed to the one thing that’ll actually kill you: a client lawsuit. I paid £1,800 for a BOP last year. My E&O policy cost £450. The BOP was a waste. Don’t be that guy. Know your risk profile. Don’t buy what’s marketed. Buy what protects you.

Astha Mishra

It is truly fascinating how the modern entrepreneurial spirit has been shaped by the illusion of simplicity-how we are drawn to bundled solutions as if they were a magic key to security, when in reality, each business carries its own unique constellation of vulnerabilities. I, myself, run a small educational consultancy from my home in Delhi, and I was initially tempted by the BOP’s promise of one-stop coverage. But then I paused. What if my client’s data is compromised through a phishing email? What if my laptop, filled with years of client notes, is stolen? The BOP, in its elegant simplicity, offers comfort-but not comprehensive protection. And comfort, in the realm of risk, can be the most dangerous illusion of all. I ended up purchasing standalone professional liability, cyber coverage, and a home-based business endorsement-each carefully chosen, each necessary. The cost was higher, yes-but so was my peace of mind. Sometimes, the path to true resilience is not in taking the easy bundle, but in having the courage to build your own shield, piece by piece.