EMI vs PI License Cost Calculator

Business Model Selection

Select your business model to calculate required capital and costs.

Choosing between an Electronic Money Institution (EMI) and a Payment Institution (PI) license in the EU isn’t just about paperwork-it’s about what your business can actually do, how much money you need upfront, and how much risk you’re willing to manage. If you’re building a digital wallet, prepaid card service, or neobank, you’re likely looking at an EMI. If you’re just moving money between accounts-like a payment processor for small businesses-you probably need a PI. The difference isn’t subtle. It’s the difference between building a bank-like product and running a payment gateway.

What Exactly Is Electronic Money?

Before you pick a license, you need to understand what sets EMIs apart. Electronic money isn’t crypto. It’s not a digital bank account. It’s money stored electronically that people use to pay others-like the balance on a prepaid card or inside a digital wallet. Under EU law (EMD2), it’s defined as a claim against the issuer, issued when you deposit real money, and accepted by someone other than the issuer. That’s why Revolut, N26, and Wise hold EMI licenses: they let users store value, send it to friends, spend it online, or withdraw it as cash. PIs can’t do that. They can only move money from one place to another. They can’t hold it.

Capital Requirements: The Big Financial Hurdle

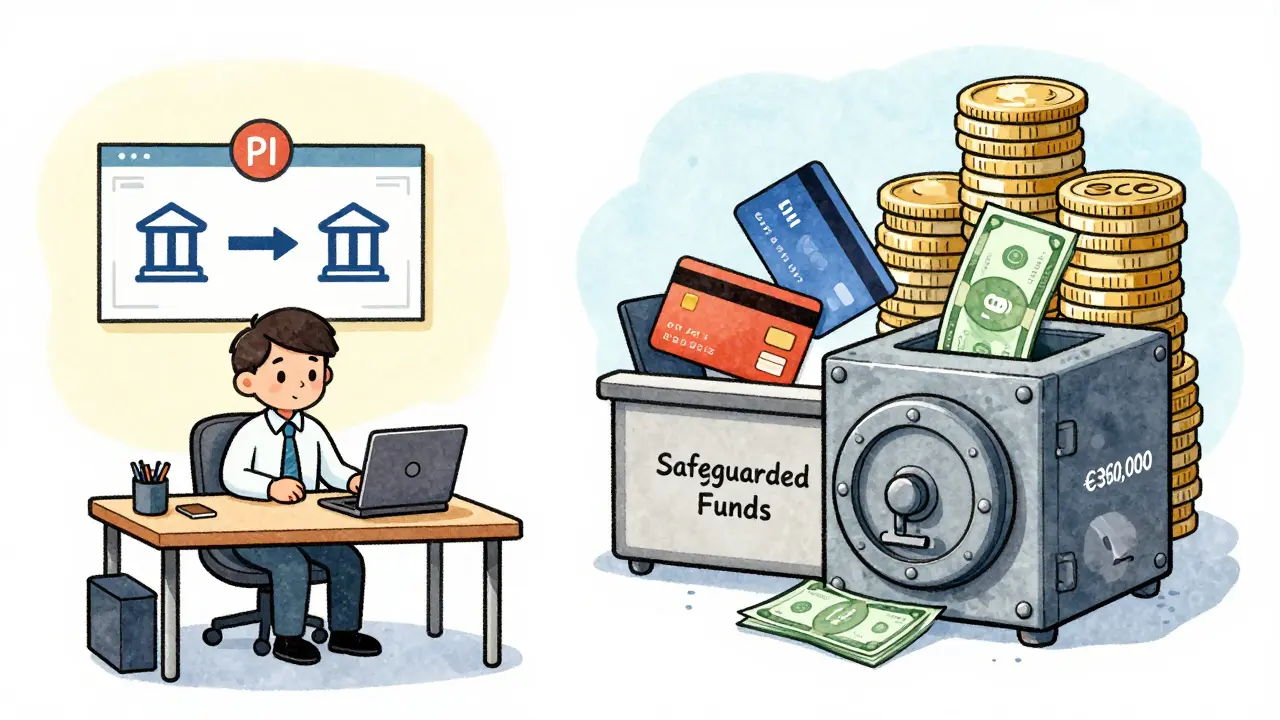

The most obvious difference between EMIs and PIs is how much cash you need to start. For a PI, the minimum is as low as €20,000-if you only offer money remittance. If you do more-like card payments, direct debits, or payment initiation-you’ll need €125,000. That’s still manageable for many startups. For EMIs? It’s €350,000. No exceptions. No lower tiers. That’s nearly 3 times more than the highest PI requirement.

But it doesn’t stop there. EMIs also have to keep 2% of their outstanding electronic money as own funds. So if you issue €10 million in e-money, you need €200,000 in extra capital on top of the €350,000 baseline. That’s €550,000 minimum. For a PI, you just need to maintain the initial amount. No ongoing percentage calculations. No surprises.

Safeguarding: Protecting Customer Money

EMIs don’t just need more money-they need to protect it differently. Every euro of electronic money issued must be fully safeguarded. That means it has to be held in a separate bank account, or invested in ultra-safe assets like government bonds. No mixing with company funds. No lending it out. No using it for operational costs. It’s locked away, ready to be returned to customers at any time.

PIs also have to safeguard client funds, but their rules are simpler. They just need to segregate money in client accounts. No 2% calculation. No mandatory investment in low-risk assets. As long as the money isn’t mixed with the company’s own cash, they’re compliant. That’s why many payment processors can operate with leaner teams and smaller compliance budgets.

What Services Can You Actually Offer?

PIs can do a lot: direct debits, card payments, bank transfers, payment initiation, account information services. But they can’t issue electronic money. That’s the wall. If you want to offer a reloadable prepaid card, a digital wallet where users keep a balance, or a loyalty program that stores value, you need an EMI. EMIs can do everything a PI can do-plus issue e-money. That’s why companies like Revolut can offer not just payments, but also crypto trading, budgeting tools, and even small loans. The wallet infrastructure gives them room to layer on services.

Most startups start as PIs. It’s cheaper. Faster. Less complex. But if you later realize you need to hold balances, you’ll have to shut down operations, reapply for an EMI license, and go through the whole €350,000+ process again. According to Aevitium’s 2023 analysis, 41% of companies that begin as PIs end up paying for a costly re-licensing later.

Regulatory Scrutiny Is Heavier for EMIs

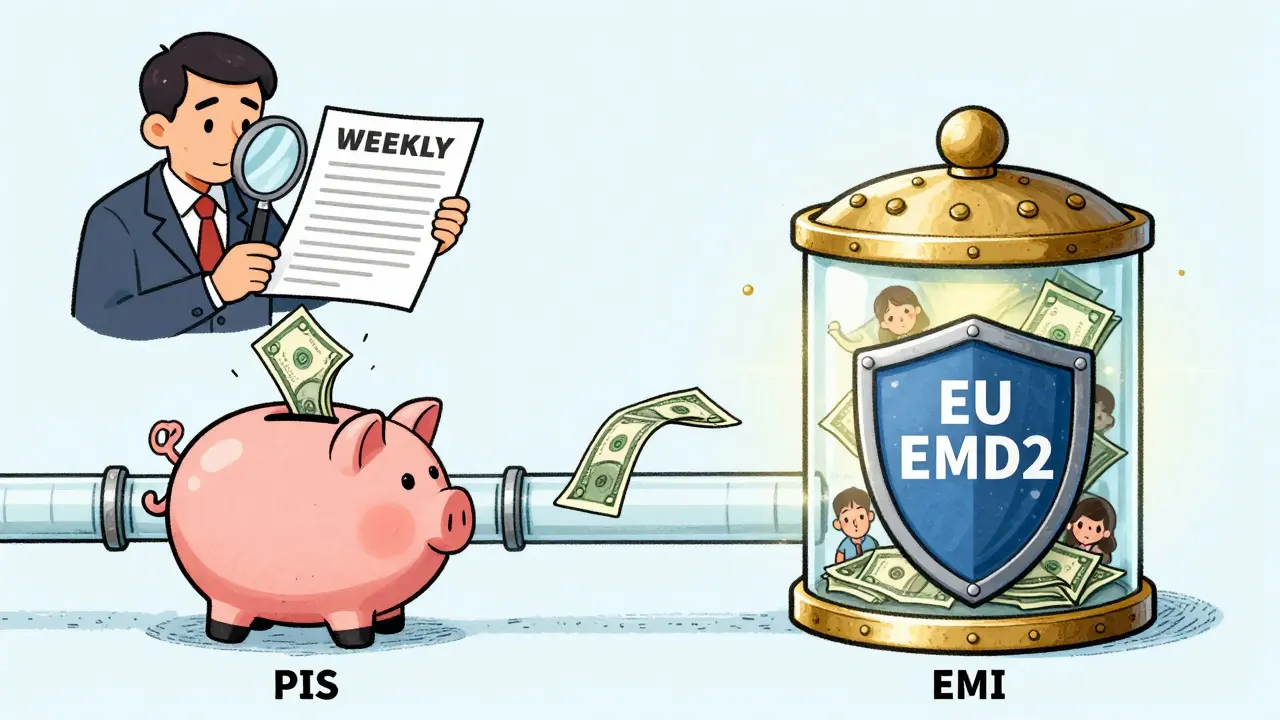

After the Wirecard scandal in 2020, regulators got nervous. EMIs, which handle stored value like quasi-currency, are now under far more scrutiny. The European Banking Authority says 63% of national regulators have tightened EMI applications since then. You’ll need rock-solid governance, detailed business plans, and flawless AML/CFT systems. Auditors will dig into your safeguarding accounts weekly now-thanks to new EBA guidelines from January 2024. PIs still face checks, but not this level.

And it’s not just paperwork. The UK’s FCA revoked 17 EMI licenses between 2021 and 2024 for safeguarding failures. Only 9 PI licenses were pulled. The risk of losing your license is higher if you’re holding money, not just moving it.

Costs and Time: It’s Not Just the Capital

Applying for either license takes 6-9 months. But EMIs cost more to prepare. Most successful applicants spend €150,000-€250,000 on legal, compliance, and tech setup before even submitting. EMIs spend 37% more on compliance infrastructure than PIs. In Germany, an EMI application costs €11,900. A PI? Around €6,150. In the UK, the difference is even starker: €5,000 for an EMI vs. €1,500-€5,000 for a PI.

Some jurisdictions are faster. Lithuania’s Bank of Lithuania processes applications in about 5-7 months. France? Over 9 months. If speed matters, location matters.

Who Wins? Revenue Potential and Market Trends

EMIs have higher barriers-but higher rewards. McKinsey found EMIs generate 2.7 times more revenue per customer than PIs. Why? Because they can offer value-added services: interest on balances, foreign exchange margins, subscription fees, embedded finance. A PI is a utility. An EMI is a platform.

Market data shows this. As of Q1 2024, there were 387 active EMIs and 1,214 PIs in the EU. But EMIs control 63.2% of all outstanding electronic money-€1.27 trillion in 2023. PIs handle far more transactions (€184.7 trillion), but each one is a tiny fee. EMIs make money from the balance, not just the transfer.

Gartner predicts that by 2026, 45% of new digital banking entrants will choose EMI licenses-even with the high cost-because wallet-based services are the future. In 2021, that number was only 28%.

What’s Coming Next? EMD3 and PSD3

The rules are changing. EMD3, effective July 2024, requires EMIs to reconcile safeguarded assets daily and meet stricter liquidity rules. The EBA now demands weekly audits of safeguarded funds. That’s a big operational lift.

PSD3, proposed in early 2024, will eliminate the lower PI capital tiers. Soon, all PIs offering multiple services will need €125,000-no more €20,000 options. That narrows the gap between PI and EMI costs, but the 2% safeguarding requirement for EMIs remains unique.

And don’t forget stablecoins. The ECB warned that some crypto-backed payment products may need both an EMI license and a MiCA license. That’s a double regulatory burden no one planned for.

Which One Should You Choose?

Ask yourself two questions:

- Do you just process payments-like moving money from A to B? → Go with a PI.

- Do you need customers to store money, reload balances, or use prepaid cards? → You need an EMI.

If you’re unsure, test your model with a PI first. But know this: upgrading later isn’t a simple upgrade. It’s a restart. You’ll lose time. You’ll lose money. And you’ll face new scrutiny.

EMIs are for builders. They’re for companies that want to own the customer relationship, not just the transaction. PIs are for operators. Efficient. Scalable. Lower risk. But limited.

There’s no ‘better’ license. Only the right one for your business.”

Can a Payment Institution issue prepaid cards?

No. A Payment Institution can issue payment instruments like debit or credit cards linked to bank accounts, but it cannot issue prepaid cards that hold stored electronic money. Prepaid cards that allow users to load and spend funds without a bank account require an EMI license under EU law. If a PI tries to offer such a card, regulators will treat it as unlicensed electronic money issuance-and shut it down.

Is the €350,000 EMI capital requirement the same across all EU countries?

Yes. The €350,000 minimum initial capital for EMIs is set by EU Directive (EU) 2009/110/EC and applies uniformly across all member states. National regulators cannot lower this amount. However, they can add additional requirements like higher own funds, local audit rules, or enhanced reporting. Some countries, like Germany and France, also charge higher application fees, but the capital floor stays the same.

Can I start as a PI and upgrade to an EMI later?

Yes, but it’s not an upgrade-it’s a full reapplication. You’ll need to shut down your PI operations temporarily, submit a new EMI application, meet the €350,000 capital requirement, and satisfy all EMI safeguarding and governance rules. The process takes 6-9 months. Many companies lose customers and revenue during this gap. Experts recommend planning for an EMI from the start if you intend to offer wallets or stored value.

What happens if an EMI fails to safeguard funds properly?

Regulators can revoke the license immediately. In the UK, the FCA revoked 17 EMI licenses between 2021 and 2024 for safeguarding failures. Customers’ money is supposed to be protected, but if funds were mixed with company assets or invested improperly, customers may lose access. In many cases, liquidators recover only a fraction of the money. That’s why regulators now require daily reconciliation and weekly audits.

Do I need a physical office in the EU to get an EMI or PI license?

Yes. Both licenses require a registered office within an EU member state. You must have real management, decision-making, and compliance functions based there. Remote directors or virtual offices won’t work. Regulators expect to inspect premises, meet key personnel, and review local governance. Lithuania and Estonia are popular because they accept foreign applicants with proper local representation, but you still need a physical presence.

Are EMIs more profitable than PIs?

Yes, on average. EMIs generate 2.7 times more revenue per customer than PIs because they can monetize stored balances through foreign exchange spreads, interest on deposits, subscription fees, and embedded financial services. PIs make money from transaction fees-often less than 1% per payment. EMIs can earn multiple revenue streams from the same customer. That’s why big players like Revolut and N26 chose EMI licenses despite the higher cost.

How does EMD3 affect existing EMIs?

EMD3, effective July 2024, requires EMIs to reconcile safeguarded assets daily instead of monthly or quarterly. They must also maintain higher liquidity coverage ratios and conduct weekly independent audits of safeguarded funds. These rules increase operational costs and demand better tech infrastructure. Existing EMIs have until the deadline to adapt. Failure to comply can lead to fines, restrictions, or license suspension.

Can a PI offer account information services?

Yes. Under PSD2, Payment Institutions are explicitly allowed to offer account information services (AIS)-meaning they can aggregate a customer’s bank account data with their consent. This is commonly used by budgeting apps and financial dashboards. However, they cannot initiate payments without a separate payment initiation service (PIS) license. Both AIS and PIS are part of the broader PI service scope under PSD2 Annex I.

Comments (3)

Omar Lopez

Let’s be clear: if you’re even considering a PI for anything beyond basic remittance, you’re already operating on a technicality. The EU regulatory framework isn’t designed for half-measures-it’s a precision instrument. EMI licensing isn’t a hurdle; it’s a filter. Those who mistake capital requirements for barriers are fundamentally misunderstanding the nature of trust in financial infrastructure. You don’t build a digital wallet like you build a SaaS tool. You build it like a vault.

The 2% safeguarding requirement isn’t punitive-it’s epistemological. It enforces ontological separation between money and asset. That’s not compliance; that’s metaphysics made operational.

And yes, the FCA’s revocations? They’re not failures. They’re corrections. The market doesn’t need more players. It needs fewer, but more rigorous ones.

Jonathan Turner

Wow. So we’re paying 3x more just so some German bureaucrat can check your spreadsheet every Monday? Meanwhile, China’s digital yuan runs on a blockchain with zero compliance staff. And you’re telling me the EU’s answer to innovation is more paperwork and €350K in dead cash? This isn’t regulation-it’s economic self-sabotage.

And don’t even get me started on ‘safeguarding.’ You mean we can’t even *invest* customer funds? In a world where 3-month T-bills yield 5%, you’re forcing fintechs to hold cash like it’s 1998? That’s not protection-that’s financial malpractice.

Meanwhile, American startups are building real products with real capital efficiency. Europe’s stuck in a regulatory time capsule. Congrats, you’ve turned fintech into a compliance seminar with a balance sheet.

Robert Shurte

There’s a quiet irony here: the very systems designed to protect consumers from financial instability are, in their rigidity, creating a new kind of instability-by concentrating power in the hands of those who can afford the capital, the lawyers, and the auditors. The EMI/PI divide isn’t just a regulatory distinction-it’s a socioeconomic one.

What does it mean, when the ability to offer a digital wallet becomes a function of balance-sheet size rather than technical ingenuity? The market doesn’t reward innovation here; it rewards access to capital. And access to capital, in turn, is a function of privilege, geography, and network.

EMD3’s daily reconciliation? It’s a technological demand disguised as a safeguard. But who bears the cost? Not the customer. Not the investor. The startup. The lone developer in Vilnius, trying to build something meaningful, now forced to hire a compliance engineer just to keep the lights on.

And yet-there’s beauty in the precision. The requirement that e-money be a claim against the issuer, not an asset on its books-that’s a philosophical anchor. It reminds us: money is not a product. It’s a promise. And promises, when broken, don’t just cost money-they cost trust.

So yes, the cost is high. The process is slow. The scrutiny is exhausting. But perhaps that’s the point: if you’re going to hold someone else’s money, you should be held to something beyond a spreadsheet. You should be held to a standard.

That standard isn’t easy. It shouldn’t be.

But it’s not about whether you can afford it. It’s about whether you understand why it exists.

And if you don’t? Maybe you shouldn’t be doing this at all.