Taxable Accounts: How to Invest Smartly Outside Retirement Plans

When you invest in a taxable account, a standard brokerage account where you pay taxes on gains and income each year. Also known as a brokerage account, it’s the go-to place for money you need before retirement age—whether it’s for a house, a trip, or just extra savings. Unlike 401(k)s or IRAs, there are no contribution limits, no early withdrawal penalties, and no required minimum distributions. But you do pay taxes on every dividend, interest payment, and profit when you sell. That’s why knowing how to structure your investments inside a taxable account matters more than you think.

Not all assets belong in a taxable account. Holding bonds or REITs here? You’ll get hit with ordinary income tax rates—sometimes over 37%—on every payout. But stocks held over a year? You pay the lower long-term capital gains rate, which can be as low as 0% if your income is under $44,625 (single, 2025). That’s why smart investors use tax-efficient ETFs, funds designed to minimize distributions by using in-kind redemptions and low turnover like VTI or SCHB instead of actively managed mutual funds. And when you do sell, tax-loss harvesting, selling losing positions to offset gains and reduce your tax bill can save you hundreds—or thousands—each year. It’s not magic. It’s math you control.

Dividends matter too. Qualified dividends get the same low tax rate as long-term gains, but non-qualified ones? Taxed as regular income. That’s why funds like VTI or VOO are better than high-yield dividend ETFs in taxable accounts unless you’re in the 0% bracket. And don’t forget about cost basis. If you bought shares at different times, you need to track each purchase. Most brokers let you choose FIFO, LIFO, or specific identification—pick the one that gives you the best tax outcome. Many people miss this and end up paying more than they need to.

There’s no one-size-fits-all strategy. If you’re young and investing for the long haul, you can afford to hold growth stocks and let compounding work. If you’re nearing retirement, you might want to shift toward tax-efficient income streams. Either way, the goal is the same: keep more of what you earn. The posts below show exactly how real people use taxable accounts—whether they’re automating investments with paychecks, rebalancing to cut taxes, or using options to hedge without triggering big gains. You’ll see tools, tactics, and mistakes to avoid—all backed by actual experience, not theory. No fluff. Just what works.

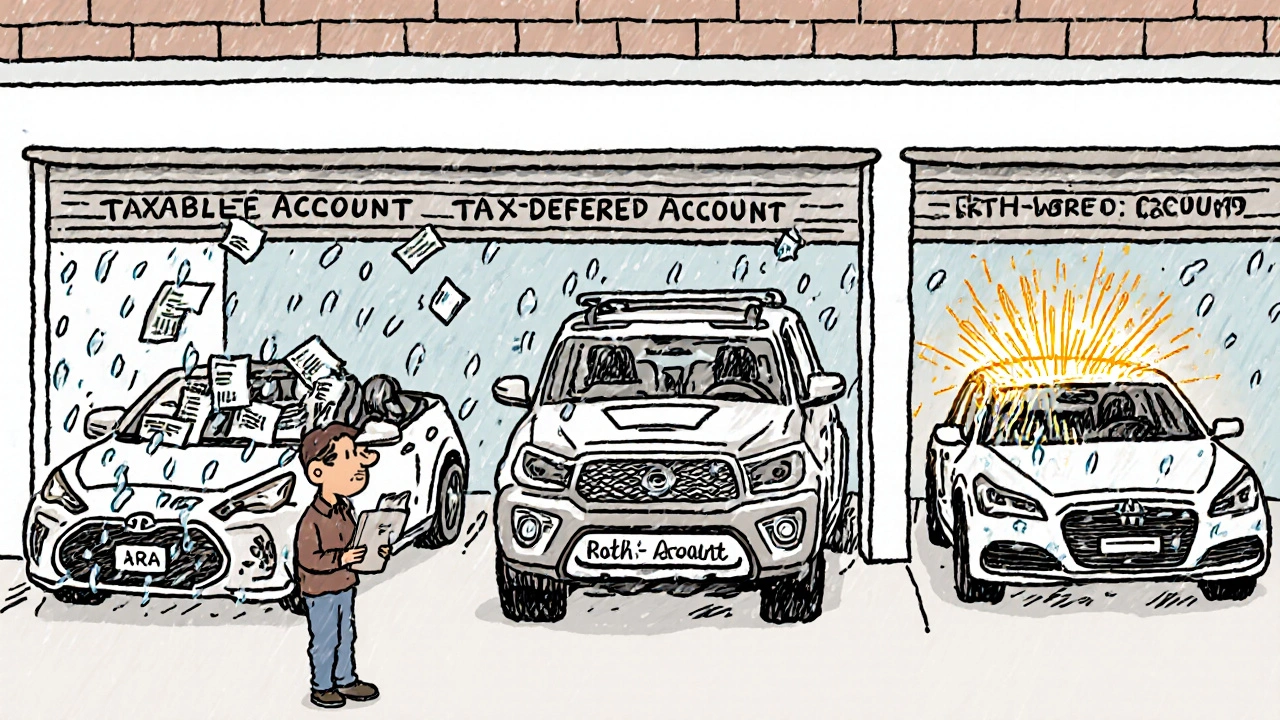

Asset Location Strategy: Put Your Investments in the Right Accounts to Keep More of Your Returns

Asset location strategy helps you maximize after-tax returns by placing the right investments in the right accounts-taxable, tax-deferred, or tax-exempt. Learn how to keep more of your gains with smart account choices.

View More