Tax-Deferred Accounts: How to Grow Wealth Without Paying Taxes Now

When you invest in a tax-deferred account, a retirement savings vehicle where you don’t pay taxes on contributions or growth until you withdraw the money. Also known as pre-tax accounts, it lets your money compound without annual tax drag—making it one of the most powerful tools for building long-term wealth. Most people think retirement accounts are just for older folks, but the real advantage comes from starting early and letting time do the heavy lifting.

Two main types dominate the landscape: the 401(k), an employer-sponsored plan where contributions come straight out of your paycheck before taxes, and the IRA, an individual account you open on your own, with options like traditional (tax-deferred) or Roth (tax-free withdrawals). The key difference? With a traditional 401(k) or IRA, you get a tax break now, but pay later when you withdraw. With a Roth IRA, you pay taxes upfront, but everything after that—growth, dividends, withdrawals—is completely tax-free. Many women in tech use both: max out their 401(k) for the employer match, then fund a Roth IRA for flexibility in retirement.

Why does this matter? Because taxes eat into returns. If you invest $10,000 in a taxable account and earn 7% a year, you’ll pay taxes on dividends and capital gains every year. In a tax-deferred account, that same $10,000 keeps growing untouched. Over 30 years, the difference can be over $100,000. That’s not magic—it’s math. And it’s why people who use these accounts consistently end up with way more than those who wait until they’re 50 to start.

But here’s the catch: tax-deferred accounts aren’t free money. They come with rules. Early withdrawals before 59½ usually trigger a 10% penalty on top of income taxes. Contribution limits change yearly—$23,000 for 401(k)s in 2025, $7,000 for IRAs. And if you’re self-employed, you can use a SEP IRA or Solo 401(k) to save even more. These aren’t just savings accounts—they’re structured tools designed to lock in discipline. The best part? You don’t need to be a finance expert to use them. Set up automatic payroll deductions, pick a low-cost index fund, and forget about it. That’s the whole point.

You’ll find posts here that show you how to pick the right account for your life stage, how to avoid common mistakes like overpaying in fees, and how to combine tax-deferred accounts with other strategies like dollar-cost averaging and partial rebalancing. Whether you’re just starting out or already maxing out your 401(k), there’s something here to help you get more out of your money—without paying more in taxes.

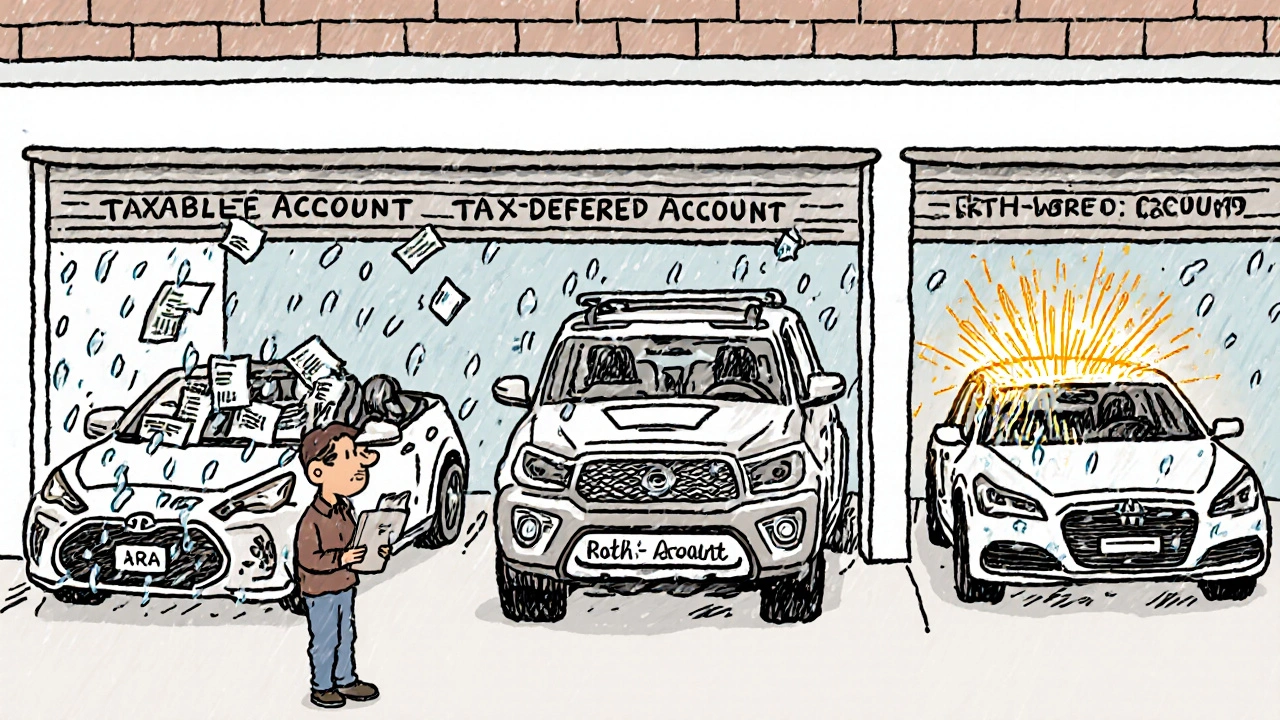

Asset Location Strategy: Put Your Investments in the Right Accounts to Keep More of Your Returns

Asset location strategy helps you maximize after-tax returns by placing the right investments in the right accounts-taxable, tax-deferred, or tax-exempt. Learn how to keep more of your gains with smart account choices.

View More