Asset Location Strategy: Where to Hold Investments for Maximum Tax Efficiency

When you’re building wealth, where you hold your investments matters just as much as what you invest in. Asset location strategy, the practice of placing different types of investments in specific accounts to minimize taxes and maximize after-tax returns. Also known as tax-efficient asset placement, it’s not about picking winners—it’s about keeping more of what you earn. Most people focus on asset allocation—how much to put in stocks, bonds, or real estate—but ignore where those assets live. That’s like buying a car and parking it in the rain without a cover.

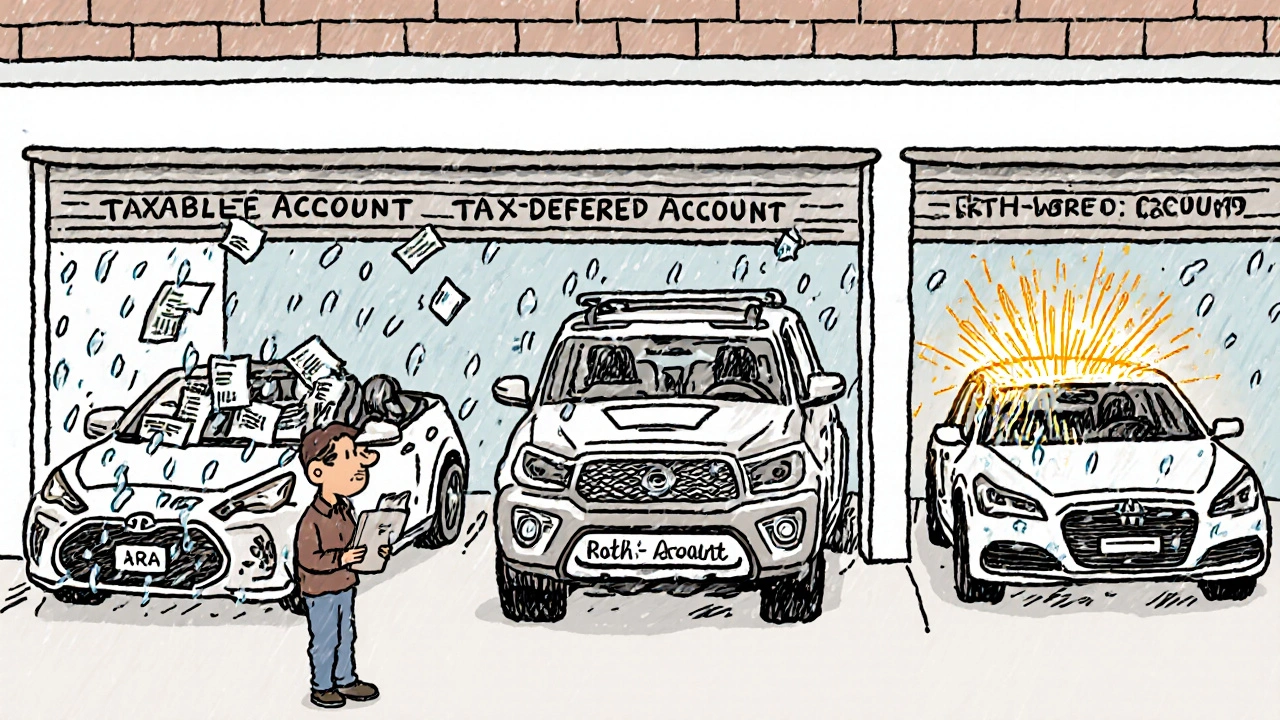

Think of your accounts as different rooms in a house. Your retirement accounts, tax-advantaged accounts like 401(k)s, IRAs, and Roth IRAs are climate-controlled spaces where growth happens tax-free or tax-deferred. Your taxable brokerage accounts, standard investment accounts where you pay taxes on dividends and capital gains each year are the garage—exposed to the elements. You wouldn’t store something fragile in the garage if you could keep it inside. So why put high-tax investments like bonds or REITs in your taxable account when you can shelter them?

Here’s how it works in practice: Bonds generate interest, which is taxed as ordinary income—often at your highest rate. Put those in your IRA or 401(k). Stocks that pay low dividends and grow over time? Those belong in your taxable account because long-term capital gains are taxed at a lower rate. ETFs that track broad markets? Perfect for taxable accounts because they’re tax-efficient by design. This isn’t theory—it’s math. A 2023 study by Vanguard showed that investors who used asset location strategy added 0.3% to 0.7% in annual after-tax returns compared to those who didn’t. That’s not a lot on paper, but over 20 years, it could mean tens of thousands more in your pocket.

And it’s not just about retirement accounts. If you’re using a Roth IRA, you’re already ahead—you pay taxes now, then everything grows tax-free forever. That’s the ultimate shelter. But if you’re putting high-growth stocks in a Roth, you’re wasting its power. Save that space for assets that would otherwise generate the most taxable income. Meanwhile, use your taxable account for the investments that naturally create less tax friction.

Asset location strategy doesn’t require fancy tools or constant tweaking. It’s a one-time setup, then a yearly check-in. You don’t need to trade often. You don’t need to time the market. You just need to know where your money sleeps. And if you’ve been putting dividend-heavy funds in your taxable account or bonds in your Roth, you’re leaving money on the table. The posts below show you exactly how to fix that—step by step, with real examples from platforms like Vanguard, Fidelity, and robo-advisors that handle this automatically. You’ll see how to spot misplacements, what to move, and when to leave things alone. No jargon. No fluff. Just clear, actionable moves that stack up over time.

Asset Location Strategy: Put Your Investments in the Right Accounts to Keep More of Your Returns

Asset location strategy helps you maximize after-tax returns by placing the right investments in the right accounts-taxable, tax-deferred, or tax-exempt. Learn how to keep more of your gains with smart account choices.

View More